U.K. Think Tank Report Criticizes International AML Reporting Regimes

First in a Three-Part Series of Blog Posts

The Royal United Services Institute (“RUSI”) for Defence and Security Studies — a U.K. think tank – has released a study: The Role of Financial Information-Sharing Partnerships in the Disruption of Crime (the “Study”). The Study focuses on international efforts — including efforts by the United States — regarding the reporting of suspicious transactions, money laundering, and terrorist financing. The Study is a critique of current approaches to AML reporting.

The Royal United Services Institute (“RUSI”) for Defence and Security Studies — a U.K. think tank – has released a study: The Role of Financial Information-Sharing Partnerships in the Disruption of Crime (the “Study”). The Study focuses on international efforts — including efforts by the United States — regarding the reporting of suspicious transactions, money laundering, and terrorist financing. The Study is a critique of current approaches to AML reporting.

In this first blog post on the Study, we will describe some of the criticisms set forth by the Study regarding the general effectiveness of suspicious activity reporting. Some of these criticisms will ring true with U.S. financial institutions, and echo in part criticisms previously raised by a detailed paper published by The Clearing House, a banking association and payments company. That paper, titled A New Paradigm: Redesigning the U.S. AML/CFT Framework to Protect National Security and Aid Law Enforcement (“The New Paradigm”), analyzes the effectiveness of the current AML and Combatting the Financing of Terrorism (CFT) regime in the U.S., identifies problems with that regime, and proposes reforms. As we previously have blogged, The New Paradigm has argued that the regime for filing SARs is outdated, that “the combined data set [from filed SARs] has massive amounts of noise and little information of use to law enforcement,” and that “the SAR database includes no feedback loop [and] . . . . there is no mechanism for law enforcement to provide feedback on whether a given SAR produced a lead or was never utilized.” These same criticisms are repeated in the Study, which looked at AML systems in the U.S, the U.K, Hong Kong, Singapore, Australia, and Canada. Although suspicious activity reporting is generally considered to be the engine which drives AML and money laundering enforcement by the government, the Study asserts: “Interviews with past and present {Financial Intelligence Units] heads as part of this project consistently raised figures of between 80% and 90% of [such reporting] being of no operational value to active law enforcement investigations.”

The Study describes itself as the product of independent research into the effectiveness of financial information-sharing partnerships in disrupting crime, in order to share good practices and to identify lessons from existing information sharing models from around the world. It begins by setting forth some “key statistics,” which — in addition to the 80% to 90% statistic noted above — include the following: (i) fewer than 1% of criminal funds flowing through the international financial system every year are believed to be frozen and confiscated by law enforcement; (ii) there is an 11% annual growth in the volume of suspicious activity reports forecasted from the major financial institutions reviewed by the Study; (iii) 85% to 95% of the financial crime control leaders polled by the study disagreed or strongly disagreed that the current framework for reporting suspicious conduct is effectively discovering and disrupting crime; and (iv) the estimated total global spend by the private sector on AML controls in 2017 was $8.2 billion. The apparent disconnect between the first three statistics and the final statistic seems particularly stark.

The Study bemoans the fact that, “[i]n all major financial markets, the number of reports of suspicions of money laundering continues to grow. Despite this, the estimated impact of anti-money laundering (AML) reporting, in terms of disrupting crime and terrorist financing, remains low.” According to the Study, “[p]art of the problem is that the private sector institutions that are asked to be the eyes and the ears of law enforcement agencies and the ‘gatekeepers’ for the integrity of the financial system have been working in the dark.” Echoing the concerns noted by The New Paradigm regarding the lack of a feedback loop, the Study finds: “Historically, private sector entities have been given little useful or timely information by public agencies with which to assess risks of money laundering or to identify suspicious activity.” The Study also suggests that contributing problems including limited law enforcement resources and expertise, which “can lead to the under[-]exploitation of existing financial intelligence,” and to the continuing issue of beneficial ownership secrecy, about which we repeatedly have blogged (here, here and here): “Effective anti-money laundering checks are often limited or prevented by the prevalence of company and trust structures, which, in a large proportion of jurisdictions, limit transparency over the ultimate beneficial owners of assets.”

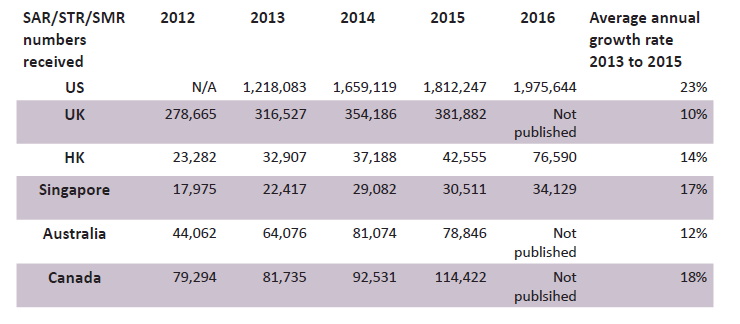

The Study also sets forth the following chart (which is replicated here, including with an apparent typographical error), regarding the amount of reports filed annually in the six countries under review regarding suspicious activity — using the particular acronyms (SAR, STR, or SMR) relevant to the particular AML reports for the various countries at issue. Bottom line: as the chart reflects, the amount of SARs filed within the United States continues to sky rocket.  The numbers set forth above beg the question: to what end are financial institutions required to file SARs? Perhaps it is the case that U.S. financial institutions are becoming increasingly more sophisticated and nuanced in detecting truly suspicious activity which always has existed, but previously was not noted and reported to the degree that it is now captured. Thus, the numbers merely reflect an improving description of reality. Alternatively, perhaps it is the case that U.S. financial institutions are feeling increasing pressure to engage in the practice of “defensive filing” — that is, the filing of SARs even when the suspicious nature of the conduct is potentially very arguable — simply in order to avoid after-the-fact questions by the institution’s regulator regarding why a SAR was not filed (because, generally speaking, no one gets into trouble with the government for filing a particular SAR, even if it is misplaced, although the opposite is certainly not true). Or, perhaps more likely, the numerical trend is explained by a mix of both scenarios. Regardless, the continuing increase in the amount of SAR filings in the United States, coupled with an increased strain on government investigative resources, suggests that any given SAR filing will receive less and less attention by government investigators, despite the best of intentions and maximum effort by everyone involved. This seems to be one of the points of the Study.

The numbers set forth above beg the question: to what end are financial institutions required to file SARs? Perhaps it is the case that U.S. financial institutions are becoming increasingly more sophisticated and nuanced in detecting truly suspicious activity which always has existed, but previously was not noted and reported to the degree that it is now captured. Thus, the numbers merely reflect an improving description of reality. Alternatively, perhaps it is the case that U.S. financial institutions are feeling increasing pressure to engage in the practice of “defensive filing” — that is, the filing of SARs even when the suspicious nature of the conduct is potentially very arguable — simply in order to avoid after-the-fact questions by the institution’s regulator regarding why a SAR was not filed (because, generally speaking, no one gets into trouble with the government for filing a particular SAR, even if it is misplaced, although the opposite is certainly not true). Or, perhaps more likely, the numerical trend is explained by a mix of both scenarios. Regardless, the continuing increase in the amount of SAR filings in the United States, coupled with an increased strain on government investigative resources, suggests that any given SAR filing will receive less and less attention by government investigators, despite the best of intentions and maximum effort by everyone involved. This seems to be one of the points of the Study.

This is not an idle question. On the one hand, creating an ever-increasing haystack does not seem to be in the best interests of government investigators combing for potentially very dangerous needles. On the other hand, how will the regulated community feel when enforcement actions are brought on the basis of the alleged failure to file individual reports which arguably have a decreasing real-world value and which are themselves not necessarily valued strongly by the regulators? The Study in part suggests — as indicated by the very title of the Study — that one path to systemic improvement is through enhanced information sharing, both between financial institutions and governments, and between financial institutions themselves.

In our next post, we will discuss the current framework for such intelligence sharing in the U.S., which is governed by Sections 314(a) and 314(b) of the Patriot Act. In our third and final post in this series, we then will discuss the findings and recommendations of the Study regarding information sharing, and how the Study believes that they will ameliorate some of the problems described above with current AML reporting.

If you would like to remain updated on these issues, please click here to subscribe to Money Laundering Watch. To learn more about Ballard Spahr’s Anti-Money Laundering Team, please click here.