The Financial Crimes Enforcement Network (“FinCEN”) has published a Small Entity Compliance Guide (the “Guide”) for beneficial ownership information (“BOI”) reporting under the Corporate Transparency Act (“CTA”), as well as updated FAQs regarding CTA compliance.

The Guide contains six chapters and an appendix. It is 56 pages long. It appears to be useful to its apparent target audience, which is small businesses confronting relatively simple issues under the CTA. The Guide is relatively clear, simply-worded and contains helpful infographics. However, what neither the Guide nor the updated FAQs does is provide any real insights into how to interpret the BOI reporting regulations. Rather, they reiterate the existing BOI regulatory requirements. Thus, anyone looking for insights into nuanced CTA issues will be disappointed.

The CTA takes effect on January 1, 2024. On that date, FinCEN needs to have implemented a working data base to accept millions of reports by newly-formed companies required to report BOI under the CTA, as well as reports by the even greater population of existing reporting companies, which must report their BOI by January 1, 2025. This is a logistically daunting task, because FinCEN estimates that over 30 million entities will need to register by the 2025 date. Perhaps one of the most interesting things about the Guidance is that it clearly asserts that the January 1, 2024 date is good, and that the CTA BOI database will be functioning by then.

That claim is debatable. FinCEN still needs to issue important and basic regulations implementing the CTA, including final rules regarding access to the data base, and proposed rules regarding how the existing Customer Due Diligence (“CDD”) Rule applicable to banks and other financial institutions might be amended – and presumably, expanded – to align with the different and often broader requirements of the CTA. Further, FinCEN’s notice and request for comment regarding FinCEN’s proposed form to collect and report BOI to FinCEN was criticized roundly. Given the backlash, FinCEN now is revising the proposed reporting form.

Similarly, on June 7, 2023 four members of the U.S. House of Representatives (the Chairpersons of the House Committee on Financial Services; the House Committee on Small Business; the House Subcommittee on National Security, Illicit Finance, and International Financial Institutions; and the House Subcommittee on Financial Services and General Government) sent a letter directed to Janet Yellen, Secretary of the Treasury, and Himamauli Das, Former Acting Director of FinCEN, regarding the status of the implementation of the CTA. The letter, fairly or not, stresses the need for transparency by FinCEN, and implies that January 1, 2024 may not be a viable date.

The fact that FinCEN devoted its limited resources to producing a 56-page publication which repeats but does not explicate current regulatory requirements for BOI reporting is unusual, given FinCEN’s many other pressing demands – such as finishing the rest of the regulations under the CTA. However, it is possible that the Guide is a reaction to demands placed upon FinCEN by certain members of Congress, who are pushing for clarity for affected businesses.

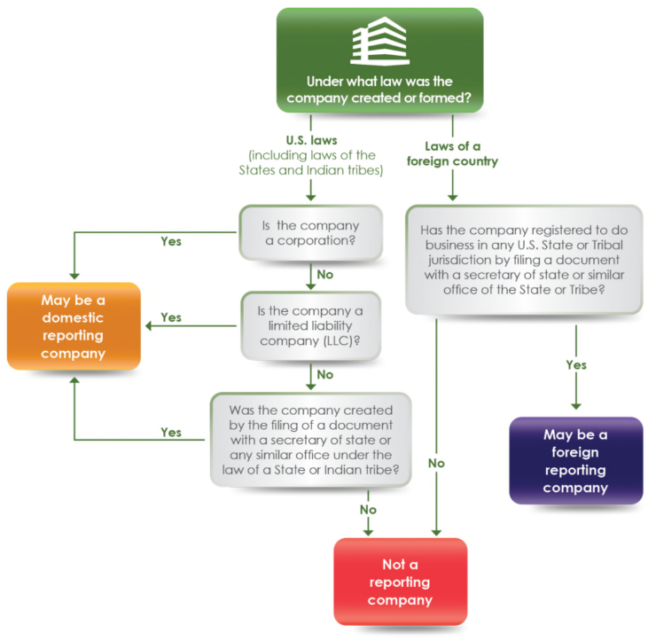

The Guide: Reporting Company

With the above caveats in mind, we now summarize the Guide. As noted, the Guide does not appear to provide additional substantive insight. Rather, it attempts to render existing regulatory requirements more accessible. For example, the Guide includes the following chart regarding the definition of a “reporting company” required to comply with the CTA:

The nuanced question to which this seemingly simple chart references, but does not expand upon, is precisely when an entity “may” be a reporting company covered by the CTA. However, the Guidance later provides a relatively useful set of questions for entities to consider as to whether they qualify as one of the 23 entities which the CTA explicitly exempts from its coverage.

The Guide: Substantial Control

The Guide also offers the following graphic regarding the issue of “substantial control” under the CTA. This is one of the thorniest issues under the CTA, given the incredible breadth of the term.

Many notable commentators have bemoaned the breadth of the vague “substantial control” prong under the CTA, in contrast to the CDD Rule, which requires entities to identify only a single “control person.” For example, Jim Richards has suggested, satirically, that his favorite bartender could qualify under the CTA as a beneficial owner of his AML consulting company, given his “substantial influence” over “important decisions” being made by Mr. Richards.

The Guide: Ownership

Similarly, the Guide provides this graphic regarding the “ownership” prong of beneficial ownership. Although the ownership interest is cabined concretely to a 25% interest, similar to the CDD Rule, the below graphic illustrates how expansively such interests may be considered:

Similar to the issue of companies exempted from the definition of reporting companies, the Guide also contains a series of yes-or-no questions regarding ownership interests under the CTA.

The FAQs

FinCEN has updated its FAQs on the CTA, first published in March 2023. Unfortunately, like the Guide, the updated FAQs provide no additional analysis, but rather regurgitate the existing CTA regulatory requirements. They note that the regulations regarding access to the CTA database are still forthcoming, and that FinCEN is still revising the actual CTA reporting form. The FAQs do not mention the regulations regarding alignment with the CDD Rule which FinCEN still needs to propose.

Having said that, FAQ D.6 is notable for certain professionals. It asks, “Is my accountant or lawyer considered a beneficial owner?” Here is the answer, which echoes language from the federal register regarding the final rule:

Accountants and lawyers generally do not qualify as beneficial owners, but that may depend on the work being performed.

Accountants and lawyers who provide general accounting or legal services are not considered beneficial owners because ordinary, arms-length advisory or other third-party professional services to a reporting company are not considered to be “substantial control” (see Question D.2). In addition, a lawyer or accountant who is designated as an agent of the reporting company may quality for the “nominee, intermediary, custodian, or agent” exception from the beneficial owner definition.

However, an individual who holds the position of general counsel in a reporting company is a “senior officer” of that company and is therefore a beneficial owner. FinCEN’s Small Entity Compliance Guide includes a checklist to help determine whether an individual qualifies for an exception.

Likewise, FAQ E.3 asks, “Is my accountant or lawyer considered a company applicant?” Again, the below language echoes verbiage from the federal register:

An accountant or lawyer could be a company applicant, depending on their role in filing the document that creates or registers a reporting company. In many cases, company applicants may work for a business formation service or law firm.

An accountant or lawyer may be a company applicant if they directly filed the document that created or registered the reporting company. If more than one person is involved in the filing of the creation or registration document, an accountant or lawyer may be a company applicant if they are primarily responsible for directing or controlling the filing.

For example, an attorney at a law firm that offers business formation services may be primarily responsible for overseeing preparation and filing of a reporting company’s incorporation documents. A paralegal at the law firm may directly file the incorporation documents at the attorney’s request. Under those circumstances, the attorney and the paralegal are both company applicants for the reporting company.

The FAQ E.3 response re-emphasizes how the CTA can pull lawyers and other professionals directly into its reporting requirements, even if they are not beneficial owners themselves.

If you would like to remain updated on these issues, please click here to subscribe to Money Laundering Watch. Please click here to find out about Ballard Spahr’s Anti-Money Laundering Team.